SHPS 30 September 2023 actuarial valuation results – what does it mean for your organisation?

Pensions

Following the SHPS valuation results, housing associations will now have decisions to make around the cost impact, longer term financial risks, your people, and your governance processes.

Join our housing experts as they lift the lid on what lies behind the SHPS results and consider what it means for the housing sector and for individual housing associations. With technical and market insight, we’ll be addressing the actions and options available to your organisation in the short, medium and longer term.

We expect housing association employers now to be focused on:

- Is the balance of investment returns and contributions right for your organisation, if not can this achieved outside of SHPS?

- Especially for those offering defined benefits, what is the right new offer for employees?

- TPT’s governance and cost management model and how this integrates with your organisation’s approach?

For new benefits being built up

- The cost of new benefits is set to go down by an average of 60% from 1 April 2025 for both Final Salary and CARE benefit structures.

- The CARE 120ths option is being removed from April 2025.

- Employers can choose to share the reduction in cost with members, pass it on in full or not at all.

There will be a premium to be paid in addition to the above rates if an employer is closed to new members.

| % pensionable salaries | Final Salary | CARE | ||||

| Accrual Rate | 60th | 70th | 80th | 60th | 80th | 120th |

| Existing future rate | 41.2% | 35.4% | 31.1% | 33.0% | 24.9% | 16.8% |

| April 2025 future rate | 16.0% | 13.8% | 12.2% | 14.5% | 11.0% | n/a |

| Net change | -25.2% | -21.6% | -18.9% | -18.5% | -13.9% | n/a |

| % Change in cost | -61.2% | -61.0% | -60.8% | -56.1% | 55.8% | n/a |

For benefits already built up

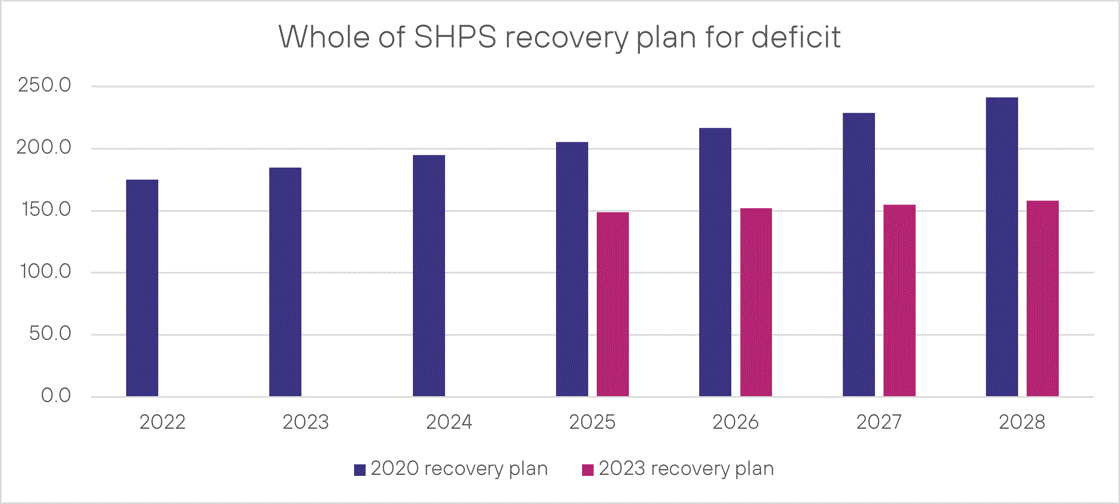

The past service deficit is more than halved – from £1.560 billion to £0.693 billion The ratio of asset to liabilities has improved by only 2% (total SHPS liabilities have approximately halved to £3.263bn, with assets also approximately halved to £2.570 billion). Annual deficit recovery contributions are set to reduce by 12% on average from April 2025 (note the actual change will vary by employer and some are increasing or will fall by more than 12%) Annual deficit contributions will increase by 2% each year rather than the current 5.5% per year The recovery plan end date remains at 1 March 2028.

Other key developments

- The valuation assumptions adopted for the 2023 valuation appear to result in higher liabilities than would have been the case has consistent assumptions been adopted. This is despite the continuing assessment of the sector’s covenant as strong.

- Expenses per employee are set to increase by around a third from April 2025 and by 60% to £126 per employee from April 2027.

- The TPT benefit review is ongoing and may add more liabilities and costs from the next valuation.

Isio support

Isio uses a “People, Finance and Governance” framework, combining actuarial analysis with wider strategic considerations to give housing associations advice to empower your Executive and Board to take informed decisions in the context of your overall business and values.

We would expect housing association employers now to be focused on three things:

1. Is the balance of investment returns and contributions right for your organisation, if not can this achieved outside of SHPS?

2. Especially for those offering defined benefits, what is the right new offer for employees?

3. TPT’S governance and cost management model and how this integrates with your organisation’s approach?

Contact us

Find out how Isio can support you.